Implementation of the Affordable Care Act (ACA) has not been without its bumps in the road. Every day there appears to be a new crisis or a new aspect exposed that suggests the Affordable Care Act was not ready for implementation. Initially, these concerns seemed to center around problems and glitches associated with the roll-out of the online healthcare.gov website. Recently however, opponents, including various news organizations, politicians, and pundits expanded their drumbeat of attacks on the ACA, claiming that President Obama knowingly lied to the American people about being able to keep their current health insurance plan, “grandfathering them in,” rather than being forced against their “will” to choose a different plan, even if their plan does not meet the minimum standards of coverage required by the ACA law.

Sound bite after sound bite has been played with President Obama telling Americans they will not have to change their plans unless they choose to do so, resulting in the added benefit of being able to continue to see the same doctor (http://www.youtube.com/watch?v=wfl55GgHr5E.) However, these statements have now been called into question. Conservatives, as well as many media organizations, have jumped on the “bash President Obama and the Affordable Care Act” bandwagon expressing their outrage at the President’s alleged audacity at intentionally misleading or lying to the American public about protections afforded consumers through the ACA as it related to keeping their current health care plan. Leading Republicans and Conservatives want the law scrapped or at the very least demand implementation of the Affordable Care Act be delayed. Recently, even some Democrats have expressed “their concern” about the promises President Obama made and indicate they are willing to consider extending the implementation of the ACA to ensure the problems are resolved. Did President Obama consistently and continually lie to the American people? Did he know that, in fact, the promises he made about people being able to keep their insurance plans, even if they were “crappy policies” or “junk policies” as the media has coined them, were allegedly false or at the very least, misleading? The evidence provided in this article will prove, beyond a shadow of a doubt, that President Obama spoke the absolute truth when he made those statements.

The Obama Administration and the authors of the Affordable Care Act recognized that people in general have a hard time with change, even if the result of the change will be positive for them (http://www4.uwm.edu/cuts/bench/change.htm). Even though health care reform will ultimately have positive consequences, a small percentage of the American people, encouraged by Conservative politicians and pundits appear to have resisted health care reform. Resistance, in general, is often based on one or more of the following factors, including but not limited to when:

- People do not fully understand why the change is needed. Many Americans believe that we have the best health care in the world. This statement is not necessarily supported by the facts. Studies suggest that the United States is now ranked 37th in the World, according to the World Health Organization (http://thepatientfactor.com/canadian-health-care-information/world-health-organizations-ranking-of-the-worlds-health-systems/).

- People feel as if they had no participation in making the change. In other words, people don’t like being told what to do just because someone said to do it. If an action is required that is preceded by “must, have to, or need to”, a person is less likely to complete the action than if they decide they “want” to change. This has proven to be true in the roll-out of the ACA state and federal health care exchanges. There are people who have been unable or unwilling to purchase adequate health insurance due to pre-existing conditions, financially out of reach premiums, lack of a belief that healthcare is a necessity, and/or lack of health insurance as an employee benefit. So much disagreement about aspects of the law have played out in the media, around kitchen tables and in the midst of social gatherings as well as political functions that nothing has been done to “fix” or resolve problem areas since the law was enacted in March, 2010. When a new law is enacted it is not unusual to have to resolve “glitches” or make process adjustments, as was the case when the Medicare Part D law took effect during the Bush Administration. It took both parties working together for the good of the American public to resolve the glitches and make other adjustments (http://crooksandliars.com/jon-perr/how-democrats-saved-bushs-medicare-drug-program).

- Jobs, power, or financial pay-outs may be in jeopardy. Stake holders may attempt to undermine the change, or in this case health care reform, as appears to have been the case with healthcare insurance executives and/or stockholders, whose salaries and financial bonuses may be reduced due to ACA rules directing that on a schedule outlined by the federal government, at least 80% of premiums collected from enrollees, must be collectively used to provide healthcare services to the enrollees by 2014. Prior to passage of the ACA, researchers determined that in many cases less than 60% of premiums were used on healthcare services for enrollees, with the rest being used for administrative costs, including but not limited to, what appears to have been excessive salaries and bonuses for upper management. (http://www.cms.gov/CCIIO/Resources/Files/Downloads/mlr-report-02-15-2013.pdf)

Based on the research associated with resistance to change, the authors of the ACA stated the following, in regard to the goal of the ACA: “The Affordable Care Act balances the objective of preserving the ability of individuals to maintain their existing coverage with the goals of ensuring access to affordable essential coverage and improving the quality of coverage.” (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34542) “Section 1251 of the Affordable Care Act provides that “nothing in the ACA requires an individual to terminate the coverage in which the individual was enrolled on March 23, 2010.” This contradicts the information provided to enrollees by letter from various insurance companies stating that due to the ACA, policies that did not offer the mandated services must be cancelled effective December 31, 2013.

This clearly proves that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan and, if it was grandfathered, then there would be no penalties imposed if a person kept their old plan. The law also provides that, “with respect to group health plans or health insurance coverage in which an individual was enrolled on March 23, 2010, various requirements of the Act shall not apply to such plan or coverage, regardless of whether the individual renews such coverage after March 23, 2010.” (Source: Overview of the Regulations: Section 1251 of the Affordable Care Act, Preservation of Right To Maintain Existing Coverage (26 CFR 54.9815– 1251T, 29 CFR 2590.715–1251, and 45 CFR 147.140) The Affordable Care Act specifically outlined how health care plans that were in effect prior to the ACA being signed into law on March 23, 2010 could be “grandfathered” and people who purchased these plans through their employment, as a part of the group or as an individual could choose to continue to be covered under their plan EVEN IF IT DID NOT MEET CERTAIN STANDARDS REGARDING ESSENTIAL BENEFITS SET FORTH BY THE ACA.

“Grandfathered” plans are defined by Bernadette Fernandez in the CRS Report R41166 as “those individual and group plans that an individual or family was enrolled in on the date of enactment (March 23, 2010).” A “grandfathered” plan may “provide for the enrolling of new employees (and their families) in such plan after March 23, 2010 as long as the plan did not cease, and someone, although not necessarily the same person was continually enrolled in the plan.” (CRS Report R41166, Grandfathered Health Plans under the Patient Protection and Affordable Care Act (ACA), Bernadette Fernandez) Simply put a person that continues with a “grandfathered” policy, from before March 23, 2010, is not subject to fines and penalties even if they do not purchase a new conforming ACA health insurance policy as long as they remain enrolled in the “grandfathered” plan. This points out again that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan and, if it was “grandfathered,” then there would be no penalties imposed.

The responsibility for gaining approval for a plan to be “grandfathered” lies strictly with the health insurance company that sold the plan. The authors of the law, as well as proponents of the law just could not have conceived that insurance companies might intentionally cease providing these policies as a means to attempt to bypass the exchanges, dramatically increasing premiums while trying to sell different plans to their customers at a much higher rate. In fact, insurance companies were given specific guidelines dictating what the insurance company had to tell consumers about the implementation of the ACA.

- If a health insurance plan was “grandfathered”, was not “grandfathered” or ceased to be “grandfathered” at some point, the insurance company was to inform the enrollee of the status of the plan, whether it met minimum ACA guidelines, offer them a choice to continue on the plan or choose to shop for a plan through the appropriate federal or state health care exchange.

- Insurance companies were also required to inform the consumer they might qualify for pre-tax incentives and/or cost-sharing subsidies if they purchase a plan through the exchange.

- Finally, enrollees had to be told that if they chose to buy a plan outside of the exchanges they would not be eligible for incentives or cost-sharing subsidies.

In the three months after the ACA was signed into law, as is typical when a new law is enacted, rules and guidelines were developed, implemented and publicized through the Federal Register that outlined what health insurance plans were eligible to be “grandfathered”, even though they did not meet the 10 new essential benefits. It also outlined what could cause a plan to cease being a grandfathered plan. “Grandfathered” plans according to “Section 1251 of the Affordable Care Act, as modified by section 10103 of the Affordable Care Act and section 2301 of the Reconciliation Act, specifies that certain plans or coverage existing as of the date of enactment (that is, grandfathered health plans) are only subject to certain provisions” of the ACA. (https://webapps.dol.gov/federalregister/PdfDisplay.aspx?DocId=23967, Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34539) The language, although somewhat confusing, clearly outlines what health care plans are eligible to be “grandfathered” based on the law as well as the conditions that insurance plans must adhere to, in order for the plan to continue to be a “grandfathered” plan including but not limited to:

- The policy had to be in force before the Affordable Care Act became law on 3/23/2010 (For the record these rules were posted June 17, 2010 so it should have been something insurance companies informed enrollees of soon after that date.) In part two of this investigative blog, which will be available by November 6, 2013 we will explore this very issue. Why weren’t enrollees informed of the status of their plan more than 30 to 60 days before the state and federal health exchanges were opened?

- No substantial financial change to the “grandfathered” plan can take place after the enactment of the ACA on 3/23/2010.

- Financial substantial change is defined as “no significant increase in a percentage cost-sharing requirement such as co-insurance”. The rules also outlined the definition of significant increase as “the maximum percentage increase is medical inflation (from March 23, 2010) plus 15 percentage points”. Medical inflation is defined in these interim final regulations “by reference to the overall medical care component of the Consumer Price Index for All Urban Consumers, unadjusted (CPI), published by the Department of Labor”. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)\

- “The employer contribution cannot decrease by five percent or more” in order to still be considered a “grandfathered” plan. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)

- “Employers and/or insurance companies cannot significantly change the dollar value of all benefits”. This could include co-insurance, deductibles, and maximum out of pocket yearly or lifetime maximums. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)

- “Substantial change to coverage cannot be made after the enactment of the ACA on 3/23/2010 including but not limited to what services, illnesses, or treatments are covered by the plan dated on or before March 2010.” (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)

- If the enrollee’s plan covered a certain condition such as asthma prior to March 23, 2010 when the ACA was enacted and the plan was “grandfathered”, changes that deleted asthma from coverage would result in a substantial change and the plan would cease to be a “grandfathered” plan.

- Substantial change could reflect an addition of a covered condition or service as well as a deletion of a covered condition or service.

The Federal Register also outlined the conditions that would result in a previously “grandfathered” plan losing its designation as a “grandfathered” plan resulting in enrollees having to purchase a different health insurance plan that would meet the guidelines of the ACA. Some of the things which could result in a health insurance plan losing this designation includes but is not limited to:

- “An increase in a percentage cost-sharing requirement” (such as coinsurance) causes a plan or health insurance coverage to cease to be a “grandfathered” health plan. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)

- “With respect to fixed- amount cost-sharing requirements other than copayments, a plan or health insurance coverage ceases to be a “grandfathered” health plan if there is an increase, since March 23, 2010, in a fixed-amount cost-sharing requirement that is greater than the maximum percentage increase. The maximum percentage increase is defined as medical inflation (from March 23, 2010) plus 15 percentage points. Medical inflation is defined in these interim final regulations by reference to the overall medical care component of the Consumer Price Index for All Urban Consumers, unadjusted (CPI), published by the Department of Labor.” (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)

- If a company tries to decrease its employer contribution to the plan its eligibility to be “grandfathered” stops. Specifically, the rules state that the employer contribution cannot decrease by five percent or more in order to still be considered a “grandfathered” plan. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34543)

- Insurance companies can’t change what services, illnesses, or treatments offered on a plan dated on or before March 23, 2010 or it is no longer a “grandfathered” policy. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations). For example, if the plan had a stated life time out of pocket maximum, employers and/or insurance companies can’t change the dollar value of all benefits or it ceases to be a “grandfathered” health plan. (Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations)

As you are probably aware, some politicians, pundits and business owners have indicated they have “had to” cut back on the hours employees work due to the expense of the ACA and/or had to offer a much more expensive health care insurance plan to enrollees based on changes made to the law by the ACA. This is simply not true. In fact, what the rules and regulations specifically state in the Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34545, is that companies CAN continue to offer a plan that existed prior to March 23, 2010 and let employees choose between what some members of the media and some politicians refer to as a “junk plan” or “plan I have always had” even if it doesn’t meet ACA guidelines. This rule clearly proves that many pundits, politicians and insurance companies are flat out lying or at the very least are flat out uninformed about the ACA when calling President Obama a liar.

This evidence points out again that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan. Perhaps these Conservative politicians and pundits, who have been so quick to call President Obama dishonest should have spent their time actually READING and STUDYING the law, as well as the guidelines and rules published in the Federal Register, before labeling President Obama as a liar.

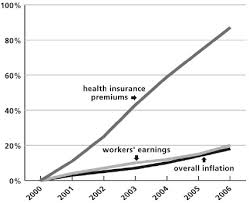

While many people call healthcare reform “Obamacare” and/or ACA (Affordable Care Act) it is important to remember neither of these two are the correct name of the law. It is actually the Patient Protection and Affordable Care Act or PPACA. (http://www.gpo.gov/fdsys/pkg/BILLS-111hr3590enr/pdf/BILLS-111hr3590enr.pdf) The law was enacted to PROTECT the health care plan consumer/enrollee as well as ensure that every American has the opportunity to obtain adequate, affordable health care insurance. Why was this necessary? Over the past several decades it appears that the percentage of the US budget being used to provide health care has sharply increased. (http://www.usgovernmentspending.com/past_spending) Premiums have risen dramatically in the past decade. The trend over the past several decades has seen employers asking employees to bear a bigger share of the health care provided. (http://www.ahrq.gov/legacy/research/empspria/empspria.htm) Due to the high cost of health insurance, many people have begun to view it as a luxury, as opposed to a necessity. PPACA/ACA establishes regulations to reign in the Health Insurance Providers from consistent and continual efforts to undermine current plans, stop the reduction of employer responsibilities in providing this benefit, and ensure the benefits provided are adequate and affordable to meet the needs of the average American worker.

It seems abundantly clear that each of the three factors described above which impact the average person’s reaction to change, along with the consistent and continual negative barrage by Conservative politicians and pundits appear to have impacted the American people’s embrace of the healthcare reform as well their understanding of the provisions and the consumer protections it offers. The ACA was intentionally structured to provide many choices for the consumers of healthcare insurance. As a result, Americans were assured they could continue with their current plan via the “grandfathered” rules, purchase a plan through the appropriate state or federal health care exchange that meets the standards outlined by the ACA, or purchase a plan by a private insurer that does not offer the potential for pre-tax subsidies and/or cost sharing. This points out again that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan.

People are more tolerant of change when they are given opportunities to make their own choices about a new concept. The authors of the PPACA law, anticipating some people’s reluctance to change health insurance plans even if it would provide them better care at a lower cost, made the decision to allow insurance companies and employers the opportunity to “grandfather” plans in place prior to the ACA being enacted on March 23, 2010. Unfortunately, it appears that intentionally or unintentionally HEALTH INSURANCE COMPANIES, negated this choice for many Americans by canceling plans that could have met the guidelines for “grandfathered” plans. Consumers across the United States indicate they have received letters, from their insurance company, indicating their health insurance plans have been cancelled effective December 31, 2013. The letters from the insurance companies seem to have some common elements:

- The enrollee is notified their plan is being cancelled effective December 31, 2013.

- The reason the plan is being cancelled is that it does not meet the requirements of the ACA.

- Enrollees are offered the opportunity to purchase a new plan, typically for a significantly higher premium which is identified and compared with their previous rate.

- Enrollees are encouraged to purchase the new plan and “lock-in” the rates before they increase again.

- Enrollees are NOT informed that they can choose to shop in the state or federal health care exchange for a plan which may include tax incentives and/or cost-sharing subsidies that may significantly decrease the cost of a health insurance plan, as well as copayments and deductibles via cost sharing.

People who have received the letters or heard about the letters appear outraged, shocked, and worried about how this will affect them. Was their worst nightmare coming true, as Republicans foreshadowed, that health insurance plan rates were going to sky-rocket and make health insurance even more unaffordable to a greater percentage of the population? While it seems to be the consensus of most people who are very familiar with the canceled plans, that these plans could be labeled as “junk plans,” canceling these health plans was entirely the decision of the insurance company since they had the option to continue offering them via the “grandfather” option under the ACA law. The insurance companies, not the requirements of the ACA law, decided that it was more profitable or less trouble to discontinue offering these policies and try to sell other, higher priced policies. The letters sent by insurance companies to enrollees informing them their plan was being cancelled, do not appear to meet these guidelines in most cases.

In fact, two insurance companies in Kentucky were investigated and fined for sending misleading instructions regarding the ACA and/or misinforming consumers about their ability to shop in the state exchange. (http://www.insurancejournal.com/topics/kentucky-humana-obamacare-letters/)(http://talkingpointsmemo.com/dc/insurance-companies-misleading-letters-obamacare) In another case in California, a Stage 4 Cancer Survivor expresses her fear, concern and abject disappointment at the negative impact the Affordable Care Act will supposedly have on her quality of care. She had been covered by a United Health Care (UHC) plan, but recently received a letter from them indicating her plan would no longer be available effective December 31, 2013.(http://thinkprogress.org/health/2013/11/04/2881581/wall-street-journal-horror-story-cancer-patient-losing-doctors-wrong/) UHC went on to explain they were pulling out of the individual health care market and she would have to find a plan through the state exchange. The exchange offered her one of two plans, but neither one allowed her keep the same provider’s she has used for her Cancer treatment. She stated, “Stanford has kept me alive—but UCSD has provided emergency and local treatment support during wretched periods of this disease, and it is where my primary-care doctors are.” (http://thinkprogress.org/health/2013/11/04/2881581/wall-street-journal-horror-story-cancer-patient-losing-doctors-wrong/) Having to choose between the doctor who saved her life and directed her treatment and the facility where she received her care seems like a cruel choice at the very least. Igor Volsky, in his article published on the website Think Progress concludes the following about UHC. “The company packed its bags and dumped its beneficiaries because it wants its competitors to swallow the first wave of sicker enrollees only to re-enter the market later and profit from the healthy people who still haven’t signed up for coverage.” He supports his premise based on a statement made by UHC Chief Executive Officer Stephen Helmsley who according to Volsky, told investors last October. “UnitedHealth will watch and see how the exchanges evolve and expects the first enrollees will have ‘a pent-up appetite’ for medical care. The company’s plans reflect its concern that the first wave of newly insured customers under the law may be the costliest.” This is just a few of the horror stories told by people who thought they would be able to retain the insurance they have had for years, but instead in ALL the cases reviewed by the authors, regardless of whether they are described here, involved the health insurance company cancelling the plan as opposed to any dishonesty by President Obama and/or members of his Administration. This points out again that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan.

Some of the letters, sent by health insurance companies to enrollees in various health care plans, contained misleading or false information about the proposed cost of plans through the federal and/or state health care exchanges prior to any announcement of what the actual cost of the plans would ultimately be. (http://talkingpointsmemo.com/dc/insurance-companies-misleading-letters-obamacare ) One pointed example in Kentucky involved enrollees in a plan offered by a large health insurance company sent letters to their enrollees telling them their plan had been cancelled due to the ACA and that they would need to purchase another plan. In addition, many health insurance companies did not adequately notify an enrollee that if they chose to purchase another plan directly from the insurance company as opposed to through the federal or state health care exchange, that tax incentives and/or cost-sharing subsidies would not be available. Finally, it does not appear that enrollees were offered the opportunity by health insurance companies or their employers to remain covered under a plan that was initially purchased prior to March 23, 2010 as afforded by the law. This points out again that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan. What President Obama or his Administration could not control was whether the insurance company chose to offer the same plan. It appears, based on preliminary evidence, that in most cases insurance companies did not choose to “grandfather” plans.

Certainly, Health Insurance Companies would not intentionally mislead the American people or would they? While it would be a terrible thing to do, it is a question that should be asked and investigated. The American people are facing a different situation now, than what has occurred in the history of the United States previously when a bill was signed into law, like the Affordable Care Act was on March 23, 2010. Examples abound throughout our history of strenuous, loud, and almost violent debates on proposed laws. But, once the bill is voted on and becomes law, our nation’s history shows that people from both political parties have come together and abided by the law, worked together to enact the law and correct problems or confusion associated with the law and did not undermine the law when it goes into effect.

For example, although there were was great push back from the public with President George W. Bush’s Medicare Part D Prescription Drug Plan along with a difficult system roll out, the Democrats worked with the Republicans in educating their constituents, answering any questions holding town meetings and supporting the law once it had passed and was implemented. (http://crooksandliars.com/jon-perr/how-democrats-saved-bushs-medicare-drug-program)

Unfortunately, this has simply not been the case with the Affordable Care Act. Even though the law was debated, changed, amended, and debated again and again prior to its passage, some members of Congress were determined, by their own admission, to do whatever it took to make this law fail, even after the law was enacted. https://progressiveandproud.wordpress.com/2013/10/05/another-acaobamacare-myth-no-negotiation-between-democrats-and-republicans-on-acaobamacare/ ) Everyday, Conservative politicians and pundits seem to take to the airwaves and gleefully tell about supposedly “new” crises about aspects of the ACA. Their refrain is the same each day, “We told you this was a bad idea.” “We told you the law was not ready to be put in force”. It reminds us of small children who when having a temper tantrum repeat over and over “told you so.” However, based on the evidence presented here it is clear that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan.

Clearly, the record shows that Conservatives have been somewhat successful in the pursuit of blaming President Obama for the problems with the roll-out of the ACA and up until today in calling him a liar about whether or not people could keep their same insurance plan, if they chose, even though it did not meet the minimum standards established by the law. History will show, we think, that the determination of Conservatives such as Mitch McConnell, Rand Paul, Paul Ryan, John Boehner, Eric Cantor, Mike Lee and Ted Cruz just to name a few, to attempt to MAKE the Affordable Care Act fail was due almost entirely to the overwhelming desire on the part of these Conservatives to keep President Obama from having any legislative success or fulfilling any of the goals he set for his Administration. This apparent rabid desire by Conservatives in opposing the Affordable Care Act is not good for the American people who will have paid an incredible price for this misplaced and misguided tenacity of opposition to the ACA. They seem willing to let the American people go untreated, even die, and when receiving treatment, potentially go bankrupt all for the ability to be able to say that the current President did not succeed. They brought our country to the brink of financial disaster in an effort to try and stop the law from being enacted. They appeared unconcerned about the $24 billion wasted in shutting down the government. It does not seem that the American people are foremost in their minds, when the American people should be the only thing in their minds. They work for the American people.

President Obama has achieved what no other President before him was able to do even though many have tried, both Republicans and Democrats. He led the pursuit for healthcare reform so that everyone in the United States would have the opportunity to have health insurance when and if needed. He stood in the gap for people like one of the authors of this blog, who developed an illness, and was unable to purchase adequate health insurance due to the presence of pre-existing illness clauses which successfully precluded people from obtaining quality health insurance. In 2011, based on the passage of the ACA, people like this author, were able to purchase affordable health insurance, prior to full implementation of the PPACA in 2014. The author credits the ACA with saving her life. Today, we, the authors, stand in the gap for President Obama, just as he did for one of the authors and many others, to report we have proven, beyond a shadow of a doubt, that President Obama told the American people the truth, that the ACA gave people currently enrolled in a particular plan on or before March 23, 2010 the choice to change plans or continue with the same pre-ACA plan. The choice WAS provided by the ACA, but the insurance companies decided that people should not have that choice. That is the bottom line.

Please Note: This blog is based on the Federal Register that is issued regularly by the Federal Government and is used in the rule making process for every aspect of the government. Preliminary, interim and final rules are published in the Federal Rules. Since the Government provides stake holders the opportunity to provide comments during the rule making process, the comments are published as well along with rationales why those comments effected changes in the rules or did not. The conclusions in this blog were solely based on information coming from the PPACA law and the implementation via the Federal Government rule making found in the Federal Register. The interim rules that are applicable to the grandfathering of policies in effect prior to the signing for the PPACA can be found in the following Federal Register. We relied on this Federal Register which defines the rules followed by the Federal Government for this content:

Federal Register section 1251 of the ACA (Source: Overview of the Regulations: Section 1251 of the Affordable Care Act, Preservation of Right To Maintain Existing Coverage [26 CFR 54.9815– 1251T, 29 CFR 2590.715–1251, and 45 CFR 147.140] https://webapps.dol.gov/federalregister/PdfDisplay.aspx?DocId=23967 , Federal Register/ Vol. 75, No. 116 / Thursday, June 17, 2010 / Rules and Regulations 34539)

By: Barbara J. Cobuzzi, MBA, CPC, CPC-H, CPC-P, CPC-I, CENTC, CPCO, Lynne Smith, MSSW and Peter J Wills, Accountant and Business Software Support Consultant.

About the Authors:

Barbara is an independent consultant in healthcare providing consulting for physicians. She is an industrial engineer from RPI with an MBA from NYU. She worked in the pharmaceutical industry for many years before moving into the healthcare industry where she had a company where she provided top quality coding, compliance and revenue cycle management services for physicians. She has since moved into full time consulting for physicians. Barbara is a nationally known expert known for her education, consulting and expert witness services.

Lynne has dedicated her career to helping others. She has experience as a social worker in a rural county, an administrator in a large hospital network and as a College Professor. She uses the skills she developed over the years as an advocate in a variety of areas including her most recent venture serving as a Healthcare Advocate. She is currently a recipient of the Pre-Existing Condition Insurance Plan, which she was able to purchase following ACA being enacted.

Together, Lynne and Barbara own the ACA Healthcare Advocates consulting firm and are available to individuals, families and businesses to help them meet the requirements of the Affordable Care Act in order to meet the specific needs of the client while optimizing the fiscal considerations.

Peter is an Accountant and Business Software Support Consultant. Prior to moving to America to marry he was an Accountant in public practice in Australia for most of his working life. For the last three years before moving here he worked as a Business Software Support Consultant for a business software developer in the housing, mining and engineering field. Peter is using his computer and business talents to assist Barbara and Lynne.

Please direct your questions and/or inquiries to askcobuzzi@gmail.com

Copyright:

© Barbara J. Cobuzzi, MBA, CPC, CPC-H, CPC-P, CPC-I, CENTC, CPCO, Lynne Smith, MSSW and Peter J. Wills, 2013. Unauthorized use and/or duplication of this material without express and written permission from this blog’s author and/or owner is strictly prohibited. Excerpts and links may be used, provided that full and clear credit is given to Barbara J. Cobuzzi, MBA, CPC, CPC-H, CPC-P, CPC-I, CENTC, CPCO, Lynne Smith, MSSW and Peter J. Wills, and The Place for Facts: Not Rhetoric with appropriate and specific direction to the original content. Permission for more comprehensive use may be obtained by contacting the authors at askcobuzzi@gmail.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Recent Comments